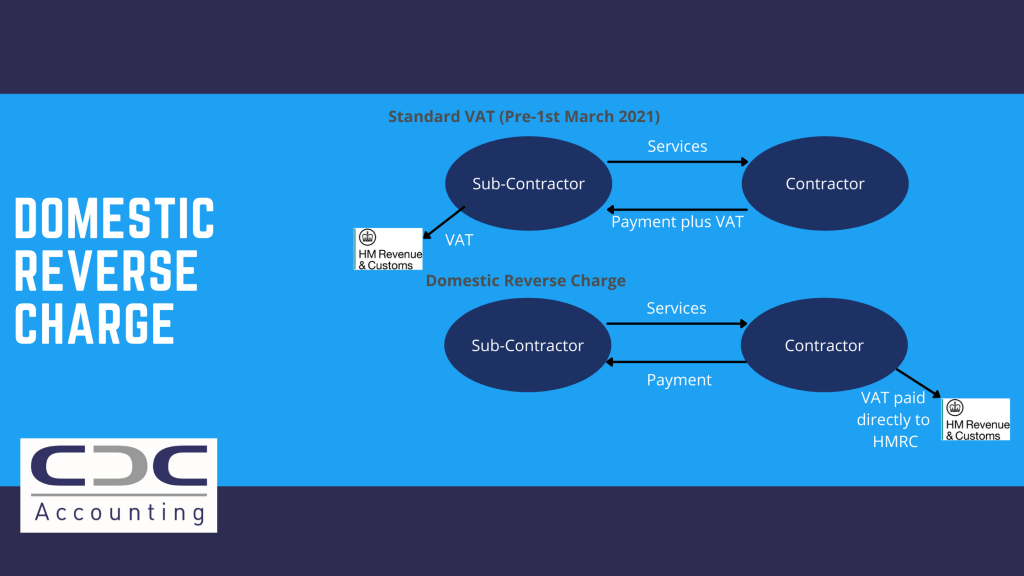

HMRC have introduced a new VAT legislation for the construction industry which comes into effect today (1st March 2021). Domestic Reverse Charge or DRC is a new way of accounting for VAT and will apply to all VAT registered construction businesses in the UK.

To sum up what this means, the Vat liability moves from the supplier (subcontractor) to the customer (contractor). The new legislation is being introduced as an anti-fraud measure designed to counter sophisticated criminal attacks on the UK VAT system. The intention is to reduce the number of 2missing trader2 fraud, where companies receive high net amounts of Vat from their customers but have no intention of paying the VAT to HMRC.

So that you understand how this new legislation will affect your business, we’ve put together a guide with key information and ways to get prepared.

Exemptions

There are some exemptions to the Domestic Reverse Charge which are as follows:

The DRC does not apply to taxable supplies made to the following customers.

- Suppliers of VAT exempt building and construction services

- Suppliers that are not covered by CIS, unless linked to such a supply.

- Suppliers of workers or staff

The reverse charge does not apply to taxable supplies made to the following customers:

- A Non-VAT registered customer

- ‘End-User’ i.e., a VAT registered customer who is not intending to make further on-going supplies of construction.

- ‘Intermediary suppliers’ who are connected e.g., a landlord and his tenant or two companies in the same group.

- Overseas customers. It only applies to UK Companies providing building and construction services in the UK.

HMRC has a detailed list of services which Reverse Charge applies to, and a full list of explanations of exemptions. Check it out here

How will DRC affect your business?

The effect DRC will have on your business depends on if you are acting as a subcontractor or a contractor. If you are a VAT-registered subcontractor (Supplier) who provides building and construction services to a VAT registered contractor (Customer) who is CIS-registered, then you no longer need to account for the VAT. You invoice should inform your customer that the VAT reverse charge is applied, and they are responsible for the VAT using the reverse charge procedure.

If you are a VAT registered Contractor (customer) you will instead account for both input and output tax on invoices you receive from your VAT registered subcontractors.

Preparing your Business – checklist

DRC is mandatory, so its important to be ready for the changes. Here are some things to consider

Software – Ensure your accounting software can deal with the new VAT domestic reverse charge. You may need to update your software to account for the DRC. If you don’t currently use accounting software, now is a good time to start. If you would like to talk through your options, then give us a call.

Cashflow – The change may affect your cashflow as you are no longer receiving the VAT payment from your customer. If you are a contractor your could have a short term cashflow benefit as you are no longer paying the Vat, however you must remember you will need to account for the VAT as an output tax as well as an input tax, along with the rest of your VAT accounting. We can help you with this if your are unsure.

Communicate – Ensuring all your staff who are responsible for the VAT accounting are aware of the reverse charge and how it will work. Contacting your subcontractors to ensure they don’t invoice you for VAT from 1st March and contacting your contract customers to make them aware you will be applying the domestic reverse charge to invoices from this date.

If you are unsure of how DRC will affect you and your business give your account manager a call and they can talk you through it.